Every year, Singapore employers are required to report their employees' earnings to IRAS. Most employers know they need to do something by March 1 — but IR8A and the Auto Inclusion Scheme (AIS) often get confused.

This guide explains what each one is, how they differ, who needs to do what, and what the deadlines actually mean for your business.

What is IR8A?

IR8A is a form that summarises an employee's total income for the year — salary, bonuses, allowances, benefits-in-kind, and any other remuneration. IRAS uses this information to pre-fill employees' personal income tax returns.

Every employer in Singapore is legally required to prepare IR8A for each employee who earned income during the calendar year. This includes full-time staff, part-time employees, and directors.

The deadline is March 1 each year, covering income from January 1 to December 31 of the previous year.

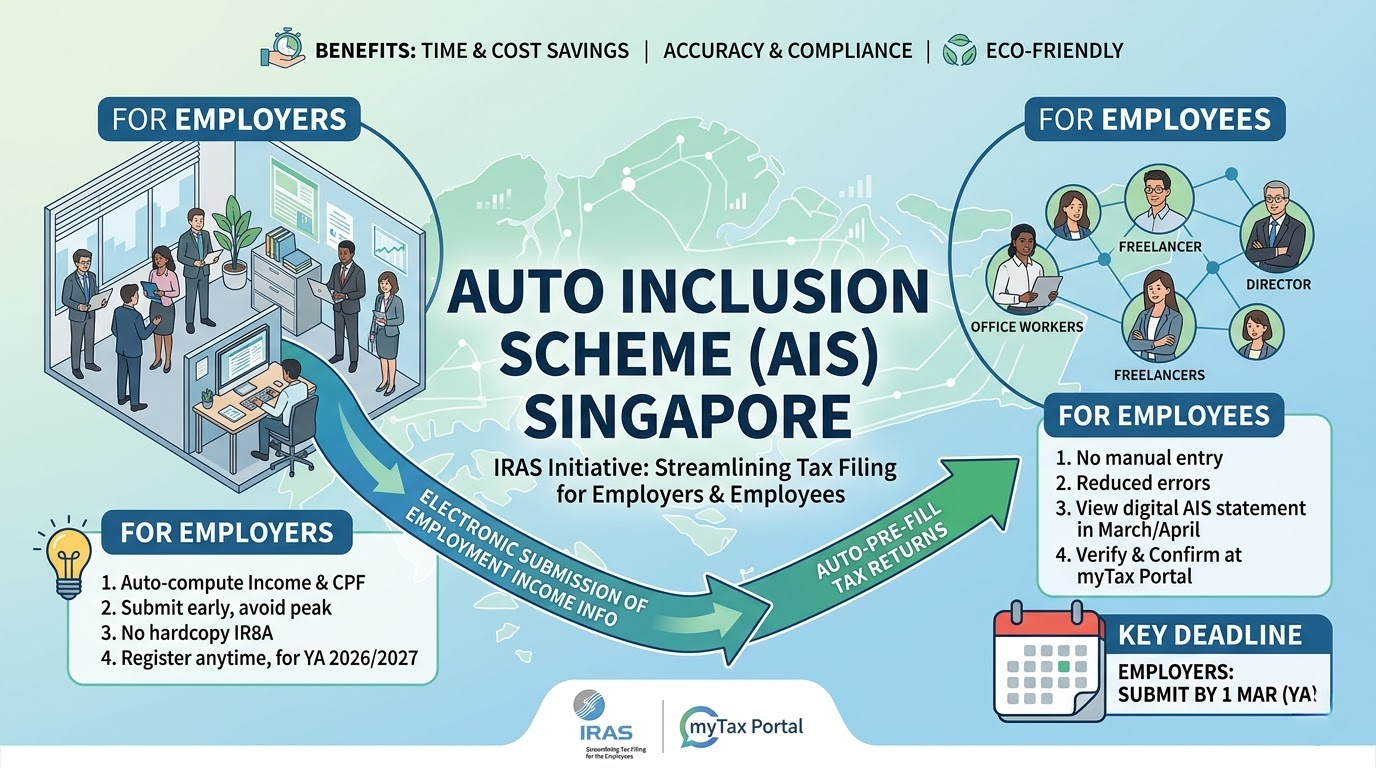

What is the Auto Inclusion Scheme (AIS)?

AIS is the electronic submission method for IR8A data. Instead of printing and handing IR8A forms to your employees, AIS participants submit the data directly to IRAS online. IRAS then automatically includes the figures in each employee's personal income tax return — employees do not need to key in their income details manually.

Think of IR8A as the data. AIS is how that data gets to IRAS.

Is AIS Mandatory?

It depends on your company size.

Mandatory AIS participation applies if your company had 5 or more employees in the previous year, or if you are a company that did not have employees but paid directors' fees.

If you fall into either category, you must submit via AIS. You cannot opt out.

Voluntary participation is available for employers with fewer than 5 employees. You can still submit via AIS, and IRAS encourages it — but if you do not, you are required to distribute physical or digital IR8A forms directly to your employees by March 1 so they can file manually.

IR8A vs AIS: The Key Differences

| IR8A | AIS | |

|---|---|---|

| What it is | The income report for each employee | The electronic channel to submit IR8A to IRAS |

| Who prepares it | All employers | Mandatory for 5 or more employees |

| Deadline | March 1 | March 1 |

| Who receives it | Employees (if not on AIS) | IRAS directly |

| Employee action required | Yes — they key in the figures themselves | No — IRAS pre-fills their tax return |

What Information Goes Into IR8A?

For each employee, you need to report basic salary, bonuses (including contractual and discretionary), director's fees if applicable, taxable allowances such as transport and meal allowances, benefits-in-kind including company car and club memberships, stock options and share awards if exercised or vested during the year, and overseas posting income attributable to work done in Singapore.

The full breakdown may require one or more supplementary forms depending on your situation.

Appendix 8A covers benefits-in-kind such as company car and accommodation. Appendix 8B covers gains from employee stock options or share plans. Form IR8S covers excess CPF contributions made by the employer. Appendix 1 applies to employees posted overseas.

You do not need all four for every employee — only the ones that apply.

Common Mistakes to Avoid

Missing part-time or short-term staff is one of the most frequent errors. IR8A applies to all employees who received income during the year, including those who left mid-year, part-timers, and contract workers. Preparing IR8A only for current full-time headcount will leave gaps.

Omitting benefits-in-kind is another common oversight. Taxable benefits like company car usage, employer-paid insurance where the employee is the beneficiary, and club memberships must be reported via Appendix 8A.

Incorrect CPF figures cause problems downstream. The CPF figures on IR8A must reconcile with what was actually submitted to CPF Board. A mismatch triggers follow-up from IRAS.

Submitting AIS data late carries penalties. The March 1 deadline is firm. If your payroll data is not finalised — for example because a year-end bonus was paid in February — you need to account for that before submitting, not after.

Not updating employee details is an easily avoidable error. IRAS cross-references submissions against NRIC and FIN numbers. Outdated or incorrect identification numbers cause submission errors and delay processing.

The AIS Submission Process

Start by finalising your payroll figures for the full calendar year from January 1 to December 31. Then prepare the IR8A data for each employee, including any applicable appendices.

Log in to myTax Portal at mytax.iras.gov.sg using your CorpPass and submit via the AIS e-Submission portal. You can upload a data file in the format specified by IRAS, or enter records manually for smaller teams.

IRAS will send a confirmation once your submission is received. Keep this for your records.

If you use payroll software, check whether it supports direct AIS submission or generates an IRAS-compatible export file. Manual data entry is error-prone at scale.

What Happens If You Miss the Deadline?

IRAS treats late or non-submission seriously. Penalties can include a fine of up to $1,000 per offence for late submission, higher penalties for deliberate non-compliance, and follow-up audits if IRAS identifies discrepancies between your submissions and employee tax returns.

If you realise you have made an error after submitting, you can file an amendment via myTax Portal. Do this as soon as you identify the mistake — voluntary correction is treated more favourably than errors flagged by IRAS.

Summary

IR8A is the income report every employer must prepare for every employee. AIS is the mandatory electronic submission channel if you have 5 or more employees. Both share a March 1 deadline.

Smaller employers not on AIS must hand IR8A directly to employees so they can file manually. Common errors — missing part-timers, omitting benefits-in-kind, wrong CPF figures — are avoidable with a checklist approach before submission.